| YTD Inventory / Shipment Report In Tons | ||

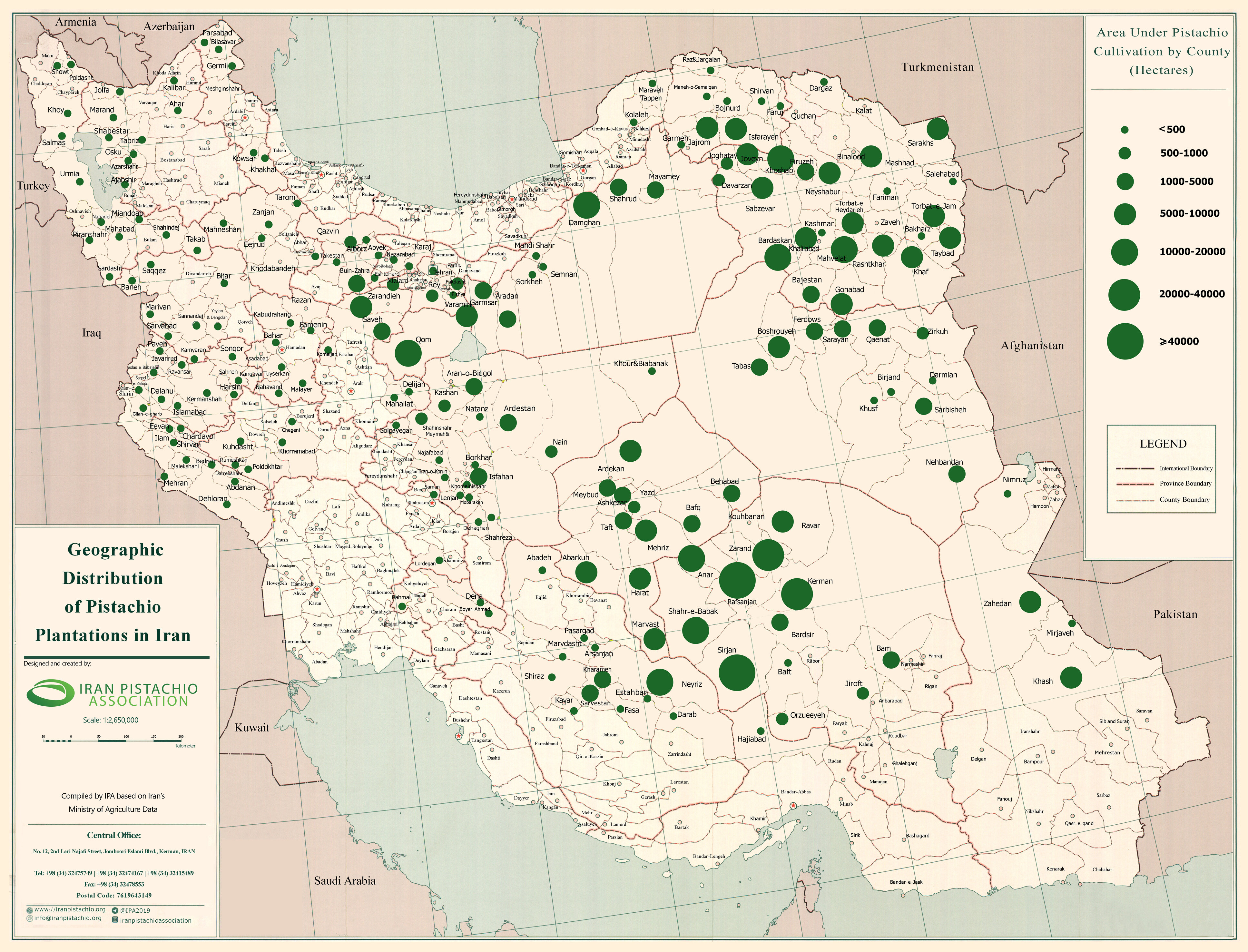

| 9th Marketing Month | Crop: 2025 | 1. Export shipments during the 9th marketing month (22 May–21 June) were at 6,000 MT of in-shell equivalent pistachios, a 45% decrease compared to the same month last year (11,000 MT). The Indian Subcontinent accounted for the largest share of monthly shipments, followed by the CIS countries and Türkiye, which mainly serves as a re-export hub. 2. Year-to-date export shipments (Sep. 2025 – June. 2026) capped at 125,000 MT of in-shell equivalent pistachios, representing a 27% decrease compared to the same period of previous year. This decline was anticipated considering war-related disruptions, operational challenges, and import restrictions in certain markets. 3. Demand in the CIS market continues to hold up well and is expected to strengthen during the summer, in accordance with typical seasonal patterns. Exports to Türkiye and the Indian subcontinent also remain strong, with their market share increasing year-on-year. 4. The Far East export share has declined significantly, from 22% through May of the last marketing year to 7% this year, following price increase of in-shell Iranian pistachios driven by strong kernel demand, as well as changes to export license regulations. Currently, in spite of strong demand for kernels and kernel raw materials in China, post-war export limitations have restricted shipments from Iran. At the same time, inventories in China are being depleted, with limited stock remaining. 5. Although war-related disruptions temporarily reduced kernel exports, shipments have significantly recovered during recent months. Under normal conditions and given the continued growth of the global kernel market, it was expected that the share of kernel shipments from total Iranian pistachio exports over the full marketing year would surpass 50% for the first time this year. However, we expect this ratio to remain around 47% for the full year, although it would still be higher than the four-year average of 41%. 6. The remaining inventory at the end of the 9th marketing month (through 21st of June) is estimated at 96,000 MT, 40% of this year's opening inventory, pointing to a record high carry-over for the Iranian pistachio industry. As Iran and other major producing countries are heading into an off-year pistachio crop, this high carry-over may be more of a blessing than a curse. 7. Iran’s 2026 crop guestimate was reported at 130,000 MT in the INC Congress. Iran Pistachio Association’s pre-harvest forecast of the 2026 crop will be released in a few weeks. Irrigation disruptions caused by country-wide electricity shortage are expected to negatively impact the upcoming off-year crop. |

| Carry in from prevoius year | 15,000 | |

| Total Production | 225,000 | |

| Gross Inventory | 240,000 | |

| Domestic Consumption | (19,000) | |

| Export Shipments | (97,000) | |

| Adjustment/losses, Export | (28,000) | |

| Total Consumption | (144,000) | |

| Remaining Inventory | 96,000 | |

| Note : addjustment / losses related to shelling and peeling process of kernels and green kernels. | ||

Current Crop Year

Monthly Report.pdf

Annual Report.pdf